Cameron Kusher, Director of Economic Research

First published 19 Jan 2023, 8:33am

The national rental market remains tight, characterised by strong demand and low supply, resulting in properties leasing rapidly.

While conditions are still tight, rental price growth slowed significantly over the final quarter of the year with no change nationally.

Median advertised rents were recorded at $480 per week at the end of 2022. Over the 2022 calendar year, national rents rose by 6.7%, up from a 4.7% increase the previous year.

Download the full PropTrack Rental Report – December 2022 quarter

While the market remains challenging for renters, few renters are moving into home ownership nor are there signs of investors returning to the market.

The latest housing finance data for November 2022 showed there was $8.3 billion in new lending to investors over the month, the lowest value since April 2021. Lending to first home buyers was $3.9 billion in November 2022, the lowest monthly value since May 2020.

Focusing on supply via investor lending, the share of total mortgage lending to investors remains below its long-term average, as it has consistently since mid-2017, resulting in fewer investment proerpties being purchased and exacerbating supply challenges.

With a low volume of stock available for rent at a time which demand for rentals remains strong and may increase further, we expect the market to remain challenging for renters seeking to lease a property.

The data within this report highlights a clear shift in demand for rentals to the capital cities (particularly the larger ones) and away from regional areas, which is a trend we expect to continue.

There remains an immense need for more rental accommodation, particularly in the major capital cities where demand is well in excess of supply.

It’s critical that we find ways to create more supply – either through increased investment or more build-to-rent projects – or we reduce demand, which seems unlikely.

Although property prices are decreasing and rents are increasing, it is significantly cheaper to be renting than paying off a mortgage in most cases. This indicates that transitioning to home ownership from renting is likely to remain a challenge for many.

Rental Price

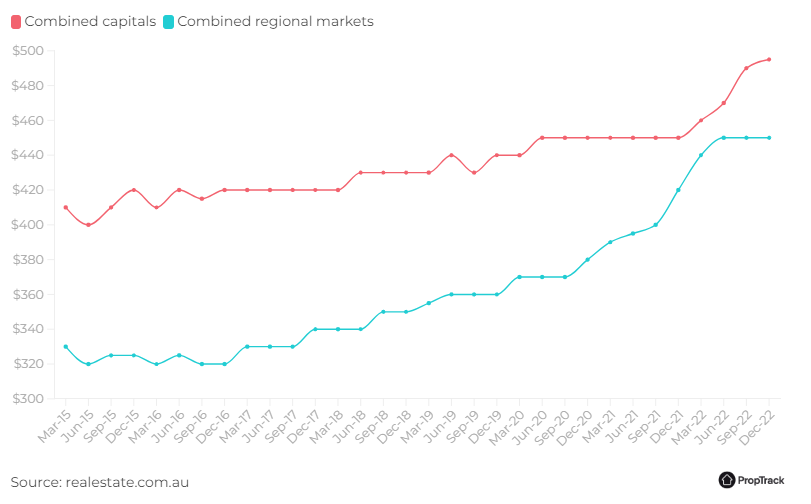

Median advertised rental prices were recorded at $480 per week at the end of 2022 and were unchanged over the final quarter of the year. They were up 6.7% higher than the 4.7% increase in 2021.

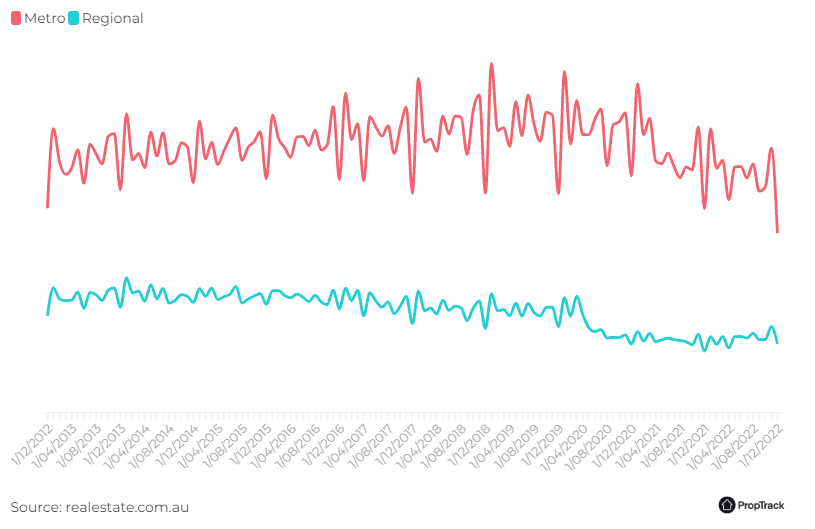

Quarterly median weekly advertised rents – capital cities vs. regional

House rents were unchanged over the quarter but increased by 7.5% over the 2022 calendar year, while unit rents rose by 2.2% over the quarter to be 9.5% higher year on year.

The annual change in house rents in 2022 was slower than the 8.1% increase in 2021, while for units, rental growth accelerated from a 1.2% decline in 2021.

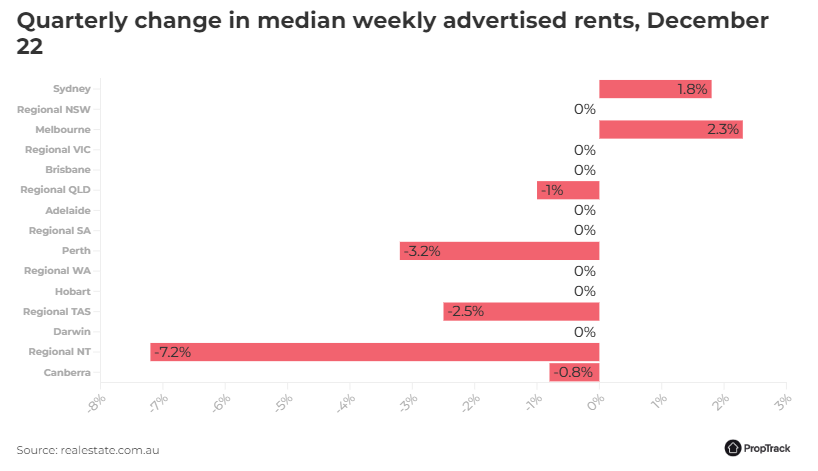

Quarterly change in median weekly advertised rents, December 22

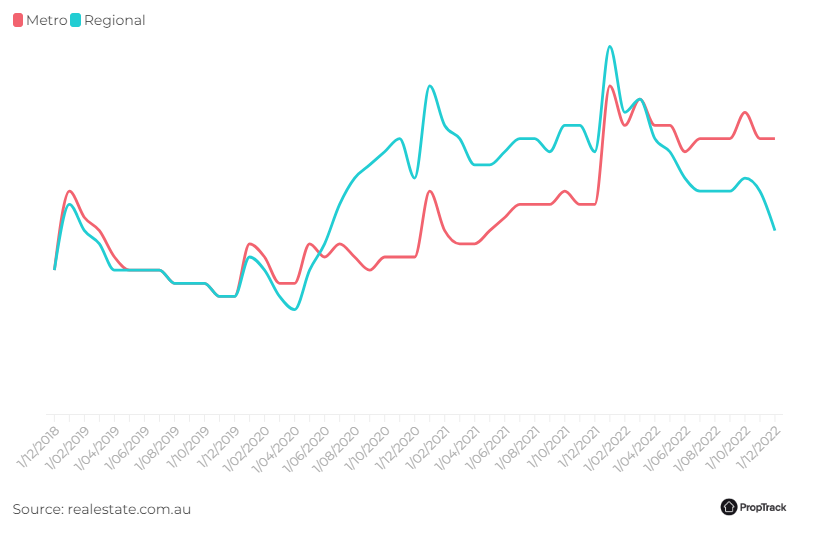

While national rents were unchanged over the quarter, combined capital city rents rose 1% to reach $495 per week and increased by 10% throughout the year.

Across the combined regional markets, rents were unchanged over the quarter at $450 per week and were 7.1% higher year-on-year. Relative to 2021, rental growth accelerated across the capital cities and slowed in regional areas in 2022.

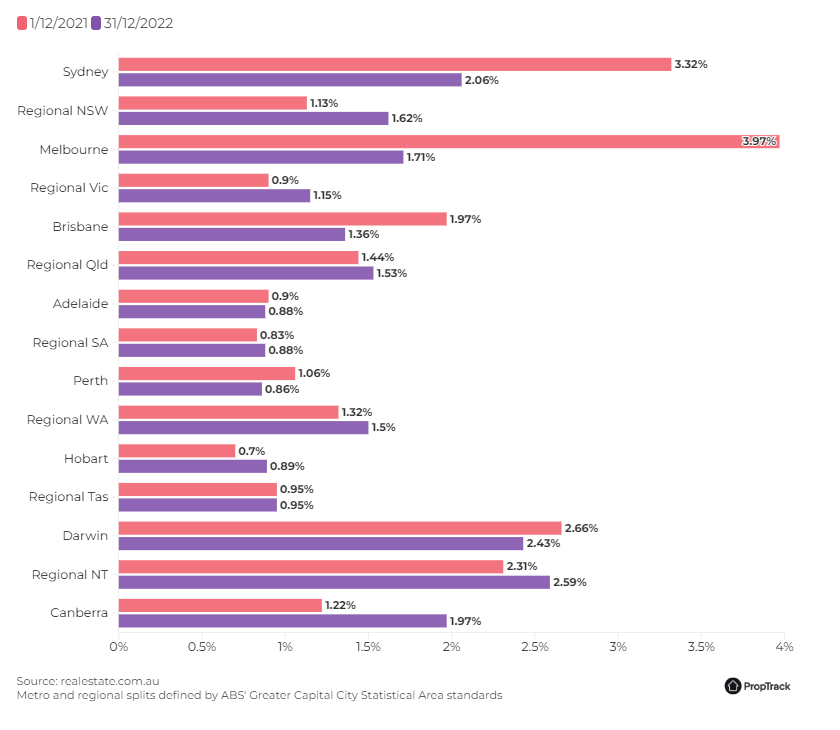

Of all the capital city and rest of state areas, only Sydney (1.8%) and Melbourne (2.3%) recorded increases in rents over the December 2022 quarter. There were large falls in regional NT (-7.2%), Perth (-3.2%) and regional Tasmania (-2.5%), with most other regions recording no change.

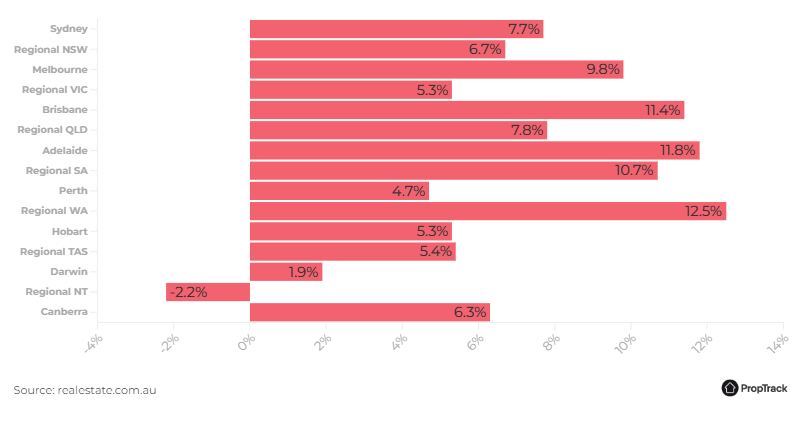

Annual change in median weekly advertised rents, December 22

Over the 12 months to December 2022, Brisbane (11.4%), Adelaide (11.8%), regional SA (10.7%) and regional WA (12.5%) recorded double-digit rental growth.

Regional NT (-2.2%) recorded a decline, with only Darwin (1.9%) and Perth (4.7%) recording rental growth of less than 5%. Compared to 2021, Sydney, Melbourne, Brisbane, Adelaide and regional SA recorded stronger annual growth in 2022, with all other regions experiencing slower growth over the past year than in 2021.

The strength in rental growth has persisted in 2022 with most regions seeing advertised rents rise by more than 5%.

However, the major capital cities are seeing the greatest price pressures, while some regional areas are seeing price growth beginning to moderate.

The weak quarterly growth will be something to monitor over the coming months. However, we expect that rents will continue to climb in the major capital cities, while the slowdown may persist in regional areas.

Rental yields

Throughout the pandemic, both property prices and rents rose, although property prices rose at a faster pace which pushed gross rental yields lower.

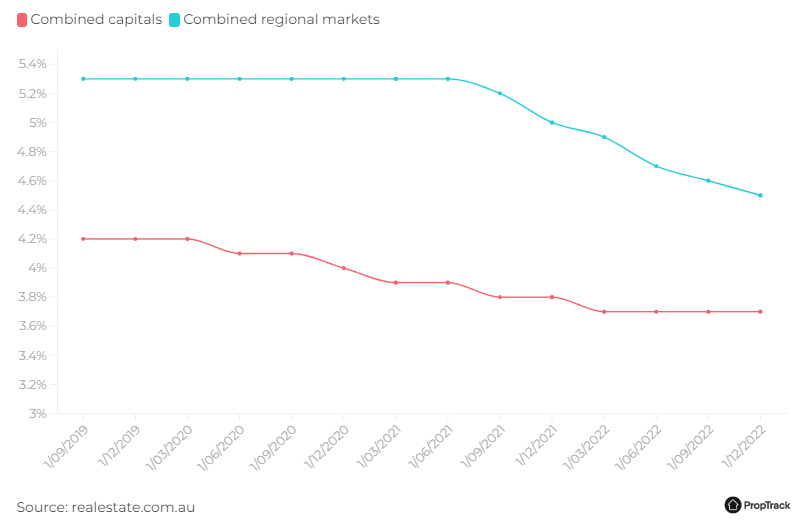

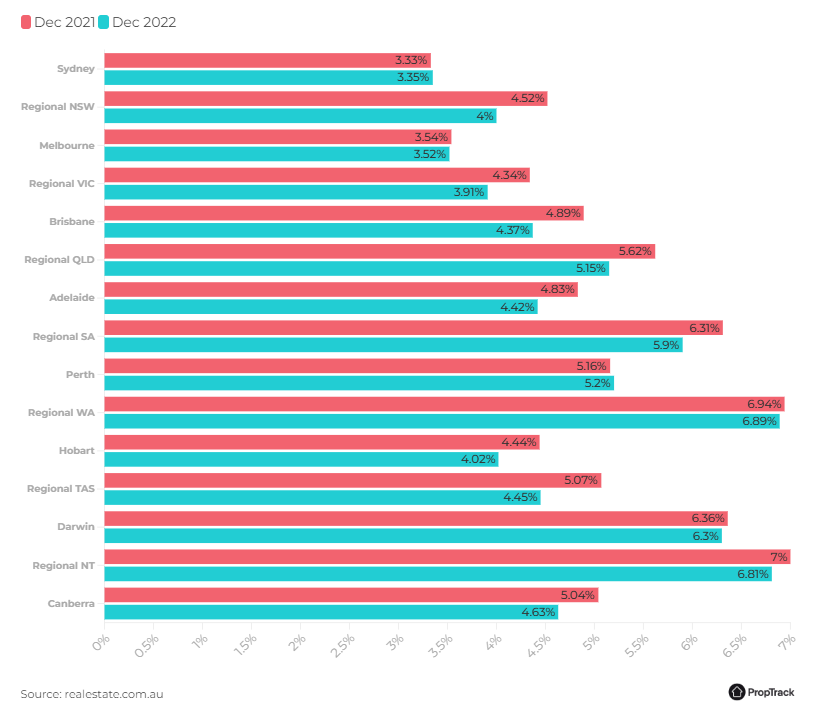

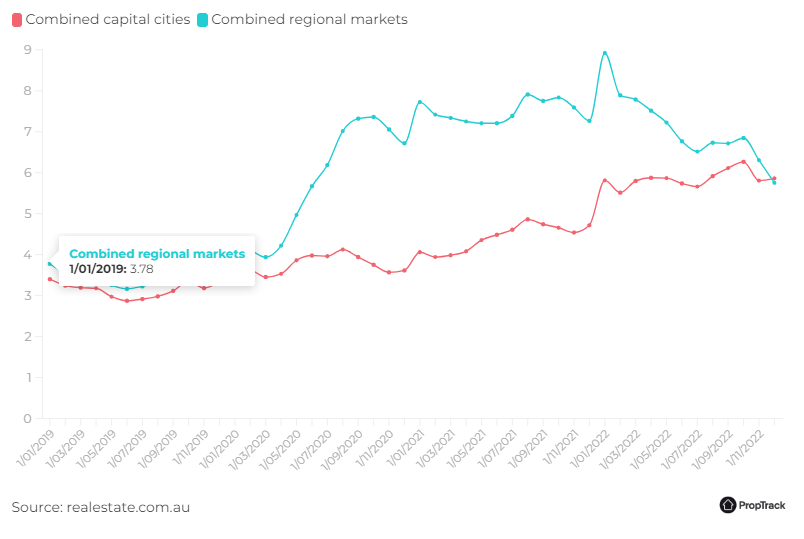

As of December 2022, gross rental yields were recorded at 3.9% compared to 4% a year earlier. Yields have started to increase over recent months as prices have fallen and rents have continued to climb.

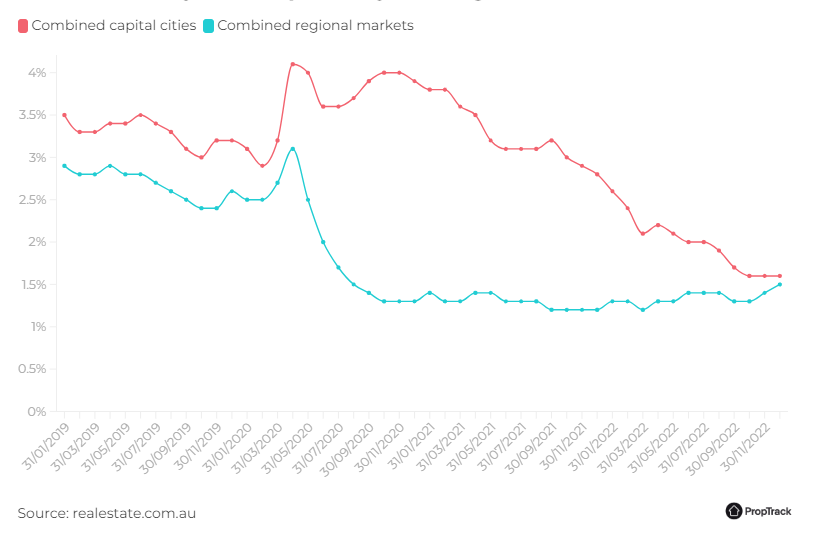

Throughout the combined capital cities, gross rental yields fell from 3.8% in December 2021 to 3.7% in December 2022. Yields have declined from 5% to 4.5% in regional areas over the same period.

Quarterly gross rental yields – capital cities vs. regional

There is a substantial variation in yield trends between houses and units. Rental yields for houses fell from 3.8% in December 2021 to 3.5% in December 2022, while unit yields increased from 4.1% to 4.3% over the year, the highest they’ve been since April 2021.

Sydney (3.3%), Melbourne (3.5%) and regional Victoria (3.9%) had the lowest gross rental yields in December 2022, while regional WA (6.9%), regional NT (6.8%) and Darwin (6.3%) had the highest yields.

Gross rental yields, December 2021 and 2022

In Sydney, Melbourne, Perth and regional WA, rental yields were unchanged compared to December 2021. Regional Tasmania (-0.6 percentage points), regional NSW, Brisbane and regional Queensland (each -0.5 percentage points) recorded the greatest softening of yields.

Mining and resource sector markets continue to have the highest rental returns, while Sydney and Melbourne and their surrounding locations overwhelmingly have the lowest rental yields in the country.

We anticipate that yields will continue to climb in 2023 as rental growth outpaces property price growth.

Rental yields remain historically low and in many cases are offering investors very little premium over term deposit rates while property prices reduce. It will be interesting to see if and how investors respond to improving yields.

New rental listings

The supply of properties becoming available for rent remains historically low, with new listings on realestate.com.au down 29.2% month-on-month in December 2022 and sitting 6.6% lower than they were in December 2021.

The number of new rental listings has been consistently lower than a year earlier since September 2022 and the number of new listings in December 2022 was the fewest since February 2010, highlighting the lack of stock available for rent.

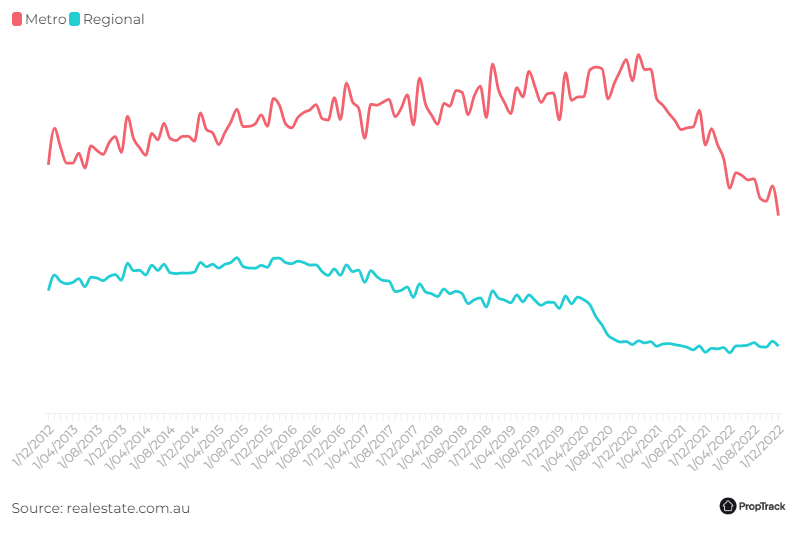

Monthly new rental listings

New supply in the capital cities is reducing, while there has been some uplift in regional areas. New listings in the capital cities in December 2022 were 12.1% lower than a year earlier, while new listings in the regional markets were 11.7% higher than during the previous December.

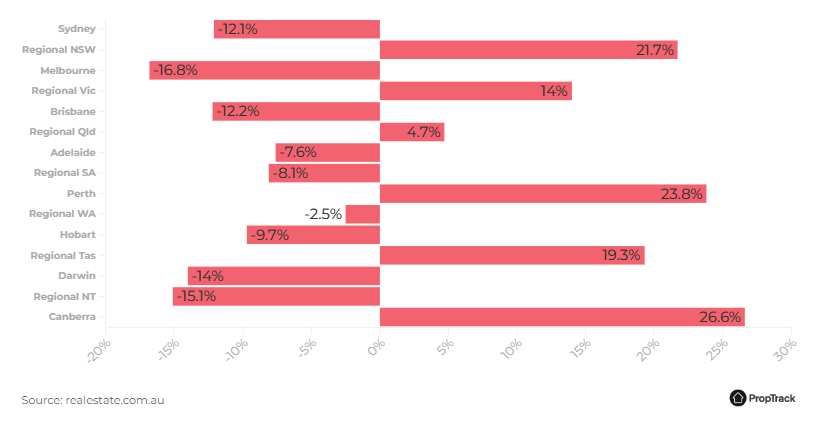

Year-on-year change in new rental listings, December 2022

The largest year-on-year increases in new rental listings were recorded in Canberra (26.6%), Perth (23.8%) and regional NSW (21.7), while the greatest declines were in Melbourne (-16.8%), regional NT (-15.1%) and Darwin (-14%).

The very low volume of new listings coming to market reflects the lack of rental stock at a time of heightened demand from renters and continues to drive significant competition for available properties.

Total rental listings

With the number of new property listings falling, there has also been an ongoing fall in total rental listings throughout 2022.

The total number of properties listed for rent on realestate.com.au fell by 11.6% month-on-month in December 2022 to be 19.5% lower year-on-year. Total rental listings remain at their lowest level since mid-2003.

Monthly total rental listings

Combined capital city total rental listings fell 13.1% month-on-month to be 26.3% lower year-on-year and are now at the lowest they’ve been since February 2003.

Throughout regional markets, total rental listings fell 6.8% month-on-month but were 9.8% higher year-on-year, their largest year-on-year increase since June 2014.

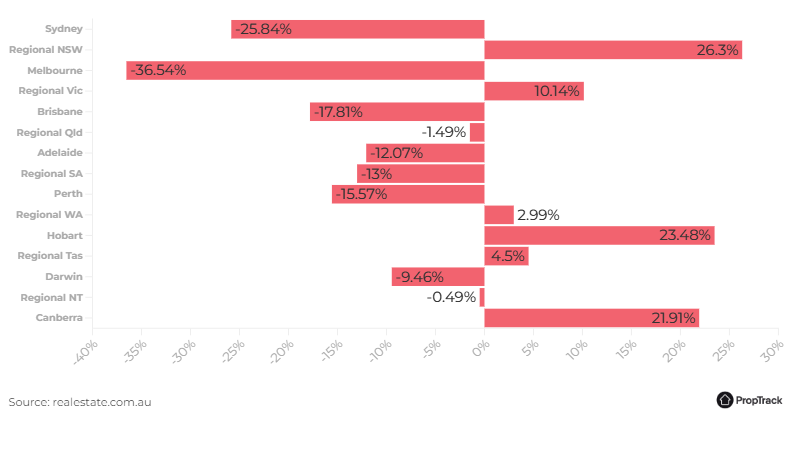

Year-on-year change in total rental listings, December 22

The most populous regions have seen the greatest falls in total rental supply over the past year, led by Melbourne (-36.5%), Sydney (-25.8%) and Brisbane (-17.8%). The greatest increases in rental stock over the year occurred in regional NSW (26.3%), Hobart (23.5%) and Canberra (21.9%).

This highlights the easing of rental market tightness in regional areas, while supply is reducing further across the major capital cities.

With the impetus to move regionally slowing and international migration lifting, most of which will be into major capital cities, we expect that the tight supply of rental stock in major capital cities will persist, putting pressure on the cost of renting.

It should be noted that although rental price growth has been strong nationally throughout the pandemic, the cost of renting in Sydney and Melbourne has seen relatively minimal growth over the period.

As a result, we expect that in these two cities, given the lack of stock available for rent, there is likely to be scope for further significant increases in rent.

Rental days on site

Properties that are available for rent are leasing in record-time due to lack of stock and heightened competition for avialable properties.

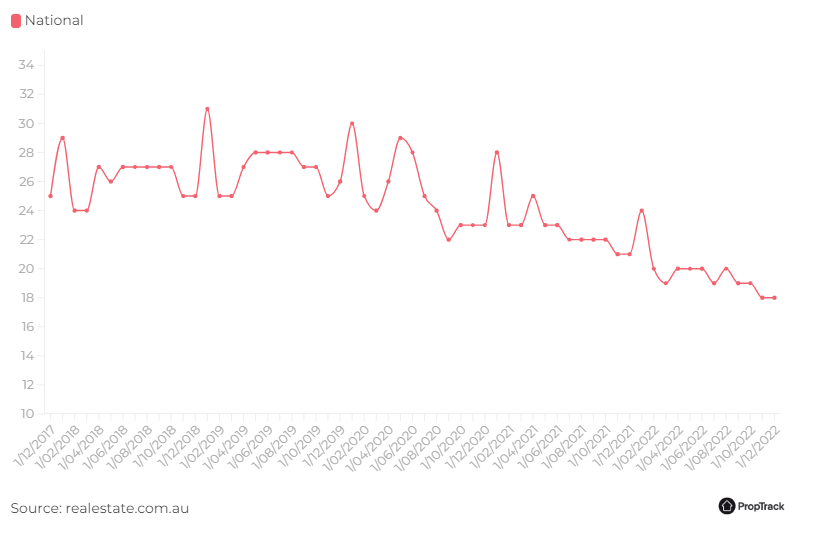

Median days on site for rental listings, National

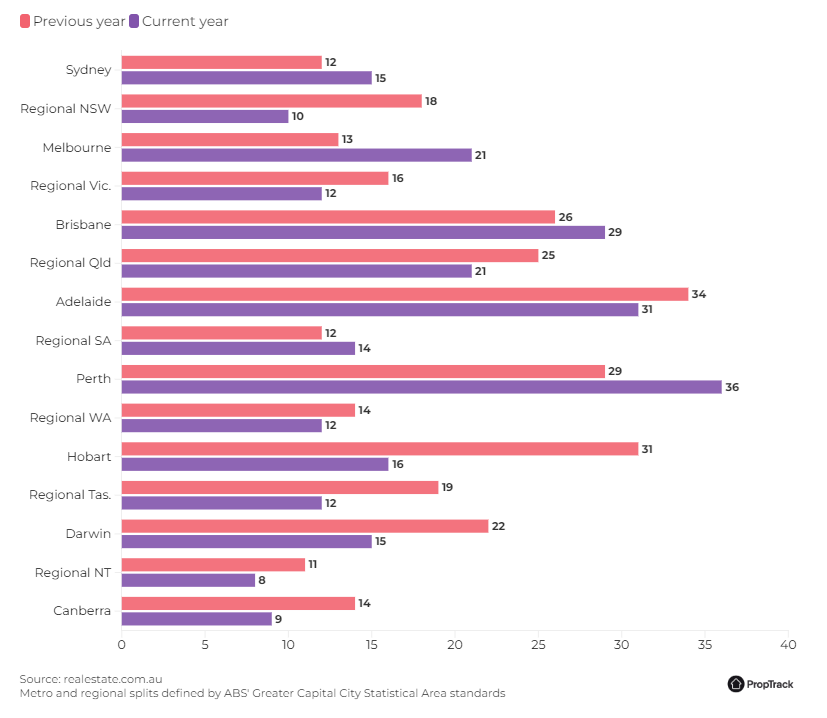

The median number of days a property was available for rent on realestate.com.au was a record-low 18 days in December 2022 compared to 19 days in September 2022 and 21 days in December 2021.

Rental days on site was lower than a year earlier in Sydney, Melbourne, Brisbane and Perth but higher elsewhere. Melbourne (-7 days), Sydney (-5 days) and Perth (-2 days) recorded the greatest falls in days on site over the year, while regional NSW (+4 days), Canberra (+4 days) and regional Victoria (+3 days) experienced the largest increases.

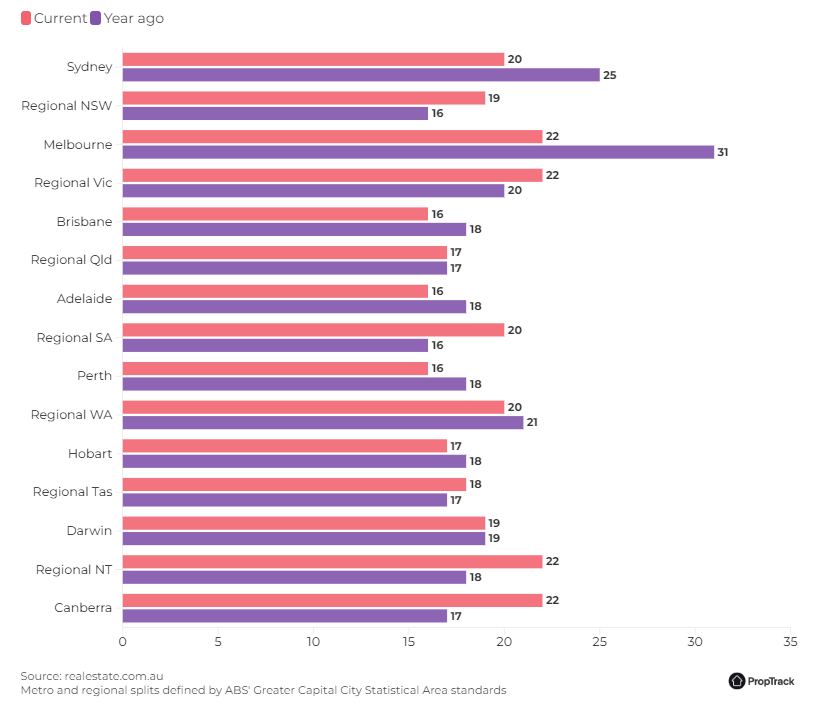

Median days on site for rental listings, December 2021 vs December 2022

Darwin (22 days), regional Victoria, regional WA and Canberra (all 21 days) currently have the longest rental days on site, while Perth (15 days), Brisbane and Adelaide (both 16 days) have the shortest.

Given the low volume of stock available for rent and heightened demand for rentals, we anticipate that rental days on site will remain at low levels over the coming months.

In fact, rental days on site is sitting at 20 days in Sydney and Melbourne and it may fall during 2023 to sit closer to the 15 or 16 days seen in the other major capital cities.

The short days on site leads to ideal leasing conditions for landlords but it makes it extremely difficult for tenants to secure accommodation given so many people are applying for each available property.

Rental vacancy rates

Over recent months, the national rental vacancy rate has been quite steady. It was 1.6% in both September and December 2022, while in December 2021 it was 2.3%.

The rental vacancy rate for houses was 1.2% in December 2022 which was steady over the quarter and year. The unit vacancy rate was 2.5%, down from 2.6% in September 2022 and 4.9% in December 2021.

Rental vacancy rate, capital city and regional areas

The combined capital city rental vacancy rate in December 2022 was 1.6%, down from 1.7% the previous quarter and 2.8% a year earlier. In regional areas, the vacancy rate rose from 1.2% in December 2021 to 1.3% in September 2022 and 1.5% in December 2022, the highest rate since August 2020.

Most regions have seen some increase in rental vacancy rates over recent months, with only Melbourne sitting at a historic low rental vacancy rate in December 2022.

Despite some recent increases, rental vacancies were lower year-on-year in Sydney, Melbourne, Brisbane, Perth and Darwin. They were unchanged in Adelaide and regional Tasmania and higher elsewhere.

Rental vacancy rates, December 2021 vs December 2022

Adelaide, regional SA, Perth and Hobart (all 0.9%) had the lowest vacancy rates in December 2022, while regional NT (2.6%), Darwin (2.4%) and Sydney (2.1%) had the highest rental vacancy rates.

The low rental vacancy rates throughout the country indicate the ongoing tightness of rental supply and the challenges renters face in finding accommodation.

Like many of the other metrics, we continue to see conditions tighten in capital city markets, while some of the rental pressures appear to be easing in the regional areas of the country.

Enquiry per listings measures key actions tenants make on a rental listing which may indicate their interest in a rental property, including by contacting the agent (via email, phone or SMS) or other behavioural indicators such as saving or booking inspection times

Enquiry per listing

On average there were 19 enquiries per rental listing in December 2022 which was up 11.8% from the previous December.

This data again highlights divergent trends between the capital cities and regional markets, with enquiry per listing rising 31.3% year-on-year across capital cities and falling 30% in regional markets.

Average key enquiry per rental listing

Rental properties in Perth, Adelaide, Melbourne and regional Queensland received the highest volume of enquiry per listing in December 2022, while regional NT, Canberra and regional NSW had the lowest volume.

Average key enquiry per listing, Dec 21 vs Dec 22

The biggest increases in rental enquiry per listing year-on-year were in Melbourne (61.5%), Sydney (25%) and Perth (24%), while the greatest falls were in Hobart (-48.4%), regional NSW (-44.4%) and regional Tasmania (-36.8%).

The average number of enquiries per listing for capital city properties was 50% higher than those in regional markets in December 2022.

A year earlier, capital city property enquiries per listing were 20% lower than enquiries in regional areas.

This highlights how much rental interest has lifted in capital cities as COVID restrictions have eased. At the same time, it highlights the slowing of demand for rental properties in regional areas.

Potential renters

The number of potential renters metric looks at how people are interacting with rental listings on realestate.com.au and determines how interested they are in a property based on those interactions.

It looks at enquiry but also measures people that have heightened interest in a property that may not have yet made contact with the agent.

The number of potential renters slowed in December which is typical over the end-of-year break. The volume was 7.2% lower year-on-year and 28.2% below its peak. Overall, demand for rentals has eased somewhat over the past year.

However, the reduction of rental supply has been greater and resulted in a 17% year-on-year increase in the number of potential renters per listing.

Potential renters per listing, capital city and regional

Somewhat surprising is the fact that the number of potential renters has recorded a larger year-on-year fall across the combined capital cities (-7.4%) than it has in regional markets (-7.1%).

When adjusted for rental supply, potential renters per listing was 27.9% higher year-on-year in capital cities and 17% lower in regional markets.

The number of potential renters was lower year-on-year across all capital city and rest of state areas, with the greatest falls in regional NT (-24.9%), Darwin (-22.5%) and regional Tasmania (-14.7%). The smallest falls were recorded in Melbourne (-3%), regional Victoria (-3.5%) and Canberra (-4%).

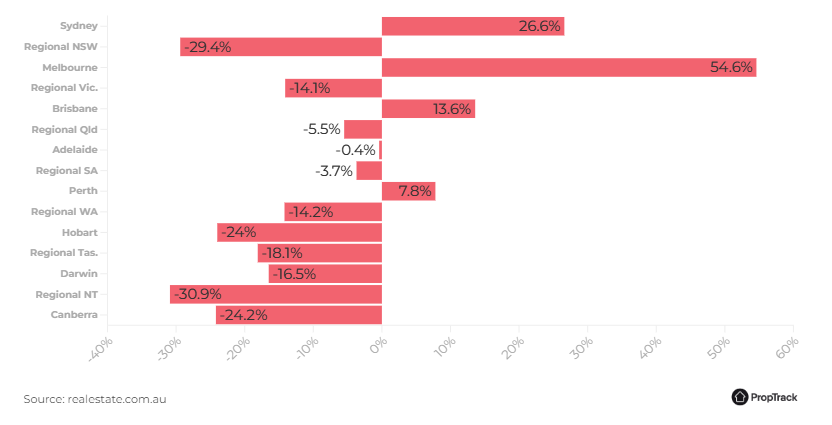

Year-on-year change in potential renters per listing, December 22

When these figures are adjusted for supply, the results are very different. The largest increases in potential renters per listing were in Melbourne (54.6%), Sydney (26.6%) and Brisbane (13.6%).

Most other regions recorded declines, the largest of which were regional NT (-30.9%), regional NSW (-29.4%) and Canberra (-24.2%).

Overall, demand for rentals is lower than a year ago. However, the lack of supply is likely to be a contributor to that easing and is further highlighted when looking at potential renters per listings.

The data is clearly showing an ongoing lift in rental demand in the capital cities, particularly the more populous ones, where the lack of stock remains a challenge.

As migration to Australia picks up further over the coming year and with the shift from renting to owning becoming much more difficult and expensive, we’re expecting ongoing challenging conditions for capital city renters.

Outlook

Some of the rental pressures that have been evident over recent years in regional markets appear to be easing, while the market is tightening in the major capital cities.

With people now returning to capital cities and overseas migration lifting, it looks as if it will become more challenging to rent a property in the capitals during 2023.

Regionally, some people that made the move during the pandemic are now planning to stay and shifting from renting into ownership and fewer people are migrating to the regions. Based on these conditions, we expect that regional rental pressures are likely to continue to ease in 2023.

In Sydney and Melbourne, the two largest rental markets in the country, it is very clear that the supply of stock for rent is reducing quickly and demand for rental properties is increasing.

Most of the overseas migration that will occur over the coming years will see those migrants settle in these two cities which will increase demand for rental accommodation.

Although supply is under- construction and build-to-rent is rising in prevalence as an asset class, it seems unlikely those additions to supply will be enough to create an equilibrium between supply and demand.

The rental market is tight, and rents have been rising because there is excess demand and insignificant supply.

With mortgage servicing costs heightened due to higher interest rates, people moving back to capital cities and overseas migration lifting, it looks unlikely that the high level of demand will reduce, particularly in capital cities.

From a supply perspective, there is a historically high volume of units under construction, some of which are build-to-rent and some have been sold to investors. However, this construction cycle has been driven by unit owner-occupier purchasers more so than in the past.

At the same time, the share of lending to investors is low and investors face higher mortgage interest costs than owner-occupiers. The most effective way to alleviate rental pressures in the short-term is to encourage more investment in housing.

Addressing the demand and supply dynamic will take some time which means that supply is likely to remain tight and the cost of renting will increase. Rent price increases will be much stronger in capital cities while regional areas are likely to see rental market pressures continue to ease.